A Brief Update on Pharmacy Benefit Managers (PBM) Reform

Pharmacy Benefit Managers (PBMs) are companies that act as intermediaries between drug manufacturers, health insurers, and pharmacies. PBMs do not directly distribute medications, but they play a pivotal role in attempting to control costs, determining quantities of medication available, and altering the overall consumer experience.

Most Americans have at some point in their lives been prescribed a medication and have been to a pharmacy to pick it up and pay for it. If this applies to you, you may have been affected by a PBM without realizing it.

As we have written, PBMs help choose which medications your doctor is allowed to prescribe and how much you will pay for them. The PBM works as a liaison between your doctor, your pharmacy, your health insurer, and the companies that manufacture and market the medication. In theory, PBMs are designed to make medicines more affordable and more accessible. But in practice, their outsized role puts PBMs in a unique position to impact the pharmaceutical market.

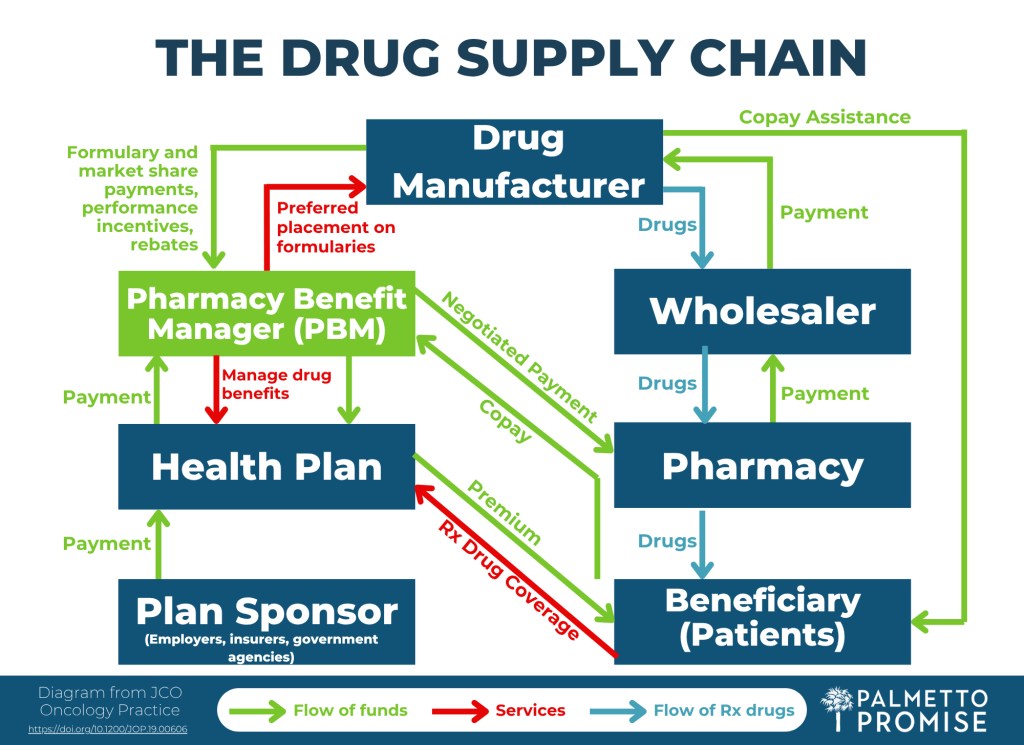

The accompanying diagram, adapted from JCO Oncology Practice and a video explanation supported by AHealthcareZ, offers descriptions of the entire drug supply chain, including the role of the PBM.

Critics would argue PBMs have unchecked power to determine the availability, cost, and access of certain pharmaceuticals. In January of 2025, the Federal Trade Commission (FTC) released the second of two scathing reports on the economic impacts of these companies. They reported PBMs generated $7.3 billion by marking up drugs in these categories over their estimated acquisition costs between 2017 and 2022, in some cases by hundreds or thousands of percent. All of this is at the expense of patients and often their insurance providers.

Here are a few ways PBMs can manipulate the costs and availability of certain pharmaceuticals:

- Rebates

-

- A PBM may have a relationship with a drug manufacturer to get paid (through rebates) in exchange for agreeing to push that medication to the exclusion of others. Instead of picking the best option, a PBM may pick the drug with the highest rebate for them.

- Spread Pricing

-

- PBMs can engage in something known as “spread pricing.” An example of this would be if a PBM agrees to pay a pharmacy $50 for a medication, but the PBM charges $60 to a client (health insurer, large employer, etc.) and then pockets the $10 difference. That adds up to a fortune.

- Owning Pharmacies

-

- When they own their own pharmacies, PBMs then have the ability to steer patients with prescriptions towards their own pharmacies. This can also disrupt small community pharmacies

- Limiting Access to “Specialty Drugs”

-

- PBMs can determine what a “specialty drug” is and which pharmacies can sell them. With their ownership stake in pharmacies, some can write into their contracts that their pharmacies are the only ones that may use these medications.

Simply put: PBMs often distort the free market rather than enhance it, and they have been allowed to operate in an opaque manner. Because they cannot see all the factors that influence the cost and quantity of medications, patients are less price-sensitive. Price sensitivity (or “demand elasticity”) means the level of desire patients have to shop around to get the best value for their dollar. This mechanism increases market competition by allowing consumers to spend their money at companies that they determine are providing them with the best quality at the best price.

Given the scale of Pharmacy Benefit Manager influence and the documented harms to patients, employers, and independent pharmacies that come with PBMs, meaningful reform is necessary. Structural guardrails are needed to restore competition and protect consumers.

Congress has begun taking steps in this direction. Bipartisan proposals such as the Pharmacy Benefit Manager Transparency Act and the Lower Costs, More Transparency Act aim to ban spread pricing, require PBMs to pass rebates directly to patients or plan sponsors, and mandate clearer reporting on how PBMs make formulary decisions. (A formulary is an official list of medicines that can be prescribed.)

States across the country have also recognized the urgency of these reforms. Ohio, West Virginia, and Oklahoma have implemented reforms that ban spread pricing in Medicaid, require transparent contracting, or establish state‑run PBM models to eliminate conflicts of interest. These efforts demonstrate that our peers are taking action.

In South Carolina, Senator Luke Rankin (R-Horry) and Representative Heath Sessions (R-York) have introduced seven pieces of legislation between them in the 2025-26 General Assembly alone (S.342, H.4790, H.4791, H.4792, H.4793, H.4794, H.4795).

Representative Sessions’ respective PBM bills focus on establishing a maximum cost list, reimbursement guidelines, and limiting coverage modifications made to certain drugs. Senator Rankin’s legislation protects smaller pharmacies from PBM reimbursements. The House legislation has bipartisan sponsorship, and several of these bills have had subcommittee hearings, which is a signal that the General Assembly may actually act at some point in the near future.

South Carolina cannot afford to wait. Legislative efforts offer the opportunity to strengthen PBM oversight and make life better for patients, physicians, pharmacists, and even insurers.