The U.S. Debt Challenge: Should South Carolinians Worry?

We frequently hear how the U.S. is in a “debt crisis.”

The U.S. Debt Clock presents debt data in real time.

Is this level of debt really a problem?

If so, what should South Carolinians do about it?

Productive Uses of Government Debt

Though most of us would prefer a smaller federal government without any debt, debt can serve legitimate purposes when used correctly.

Borrowing allows the government to continue operating despite revenue volatility (e.g., tax collections are uneven—think, April 15). During certain economic cycles (e.g., recessions), debt can be used to avoid sudden tax hikes or abrupt cuts to essential operations. It also enables funding of large capital projects like highways, ports, or military programs whose benefits will live on for decades or more.

In moments of national emergency (wars, pandemics, natural disasters), borrowing provides immediate resources when urgently needed. The federal government issues United States Treasury securities (debt) to raise this cash. The U.S. dollar is used as the world’s reserve currency, given that nearly 60% of global foreign reserves are in U.S. dollars. Further, it is used for over half of world trade transactions. In addition to holding U.S. dollars, U.S. Treasurys are a key mechanism for foreign nations to invest in U.S. dollars.

These are the defensible uses of debt. The problem arises when borrowing becomes the default tool for routine spending, political avoidance of hard choices, and the expansion of government far beyond its constitutional boundaries. That is the fiscal environment we face today.

Understanding Debt-to-GDP and Why It Matters

Debt-to-GDP is a straightforward metric: the total federal debt divided by the size of the economy. However, Debt-to-GDP is only the federal debt and does not include debt held by other entities like states, counties, firms, or households. National debt is huge already, but including these other debts, we owe even more.

Debt-to-GDP is a way to gauge whether a nation’s economy can support its obligations. Consider a household that has some debt and income. If either its debt grows too high or its income falls too much, the household cannot pay its bills. While bankruptcy might be an avenue for an insolvent household, the U.S. cannot simply declare bankruptcy. Instead, creditors would stop lending to the United States government, our interest rates to borrow would skyrocket, and the U.S. would need to sell assets to raise capital (think: sell a state) or print more money to pay the debt (think: Weimar Republic, rapid inflation).

Not a pretty scenario.

A growing economy can sustain more debt; a stagnant one cannot. Yet the metric has limitations. It doesn’t distinguish between productive investment and wasteful spending, nor does it capture unfunded liabilities such as Social Security and Medicare, obligations that dwarf the official debt and represent the true long-term fiscal challenge we face as a nation.

Counting those unfunded liabilities, U.S. obligations are roughly double what is reported.

Where the United States Stands Today

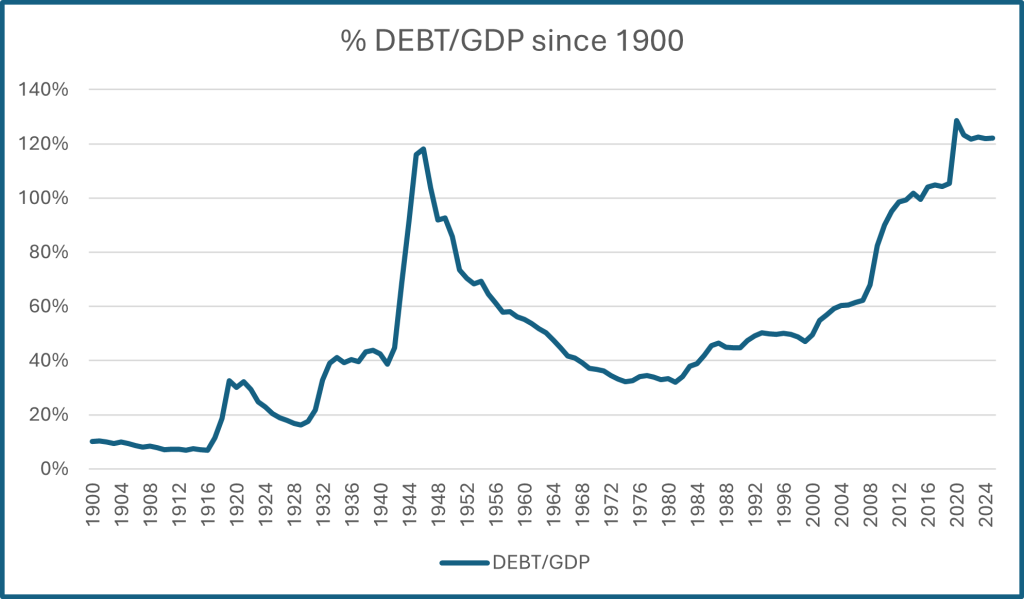

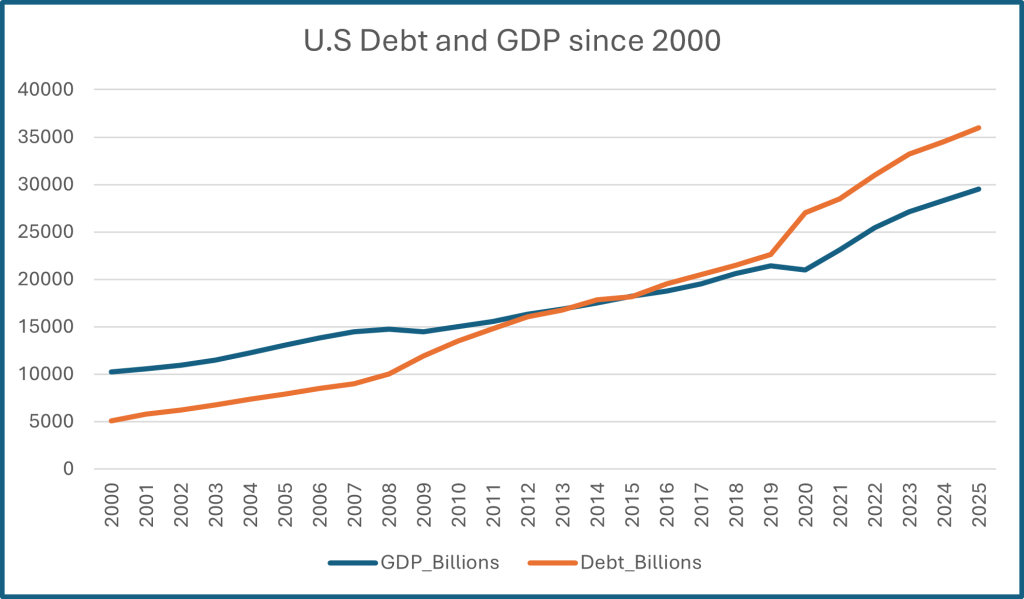

Current estimates place U.S. federal debt at roughly 121–124% of GDP, depending on methodology. In nominal terms, the national debt exceeds $38 trillion, and interest payments are among the fastest-growing components of the federal budget. Debt held by the public continues to rise, and the trajectory is unmistakably upward.

For those who prefer small government, the concern is not only the size of the debt but the structural forces driving it: entitlement spending, interest costs, and a political system that treats deficits as background noise rather than a warning siren.

How We Got Here: A Historical Perspective

The United States has had high debt before, but only under extraordinary circumstances. During World War II, debt exceeded 100% of GDP as the nation funded wartime activities. We now exceed that, but without a war. The graph shows periods of great increase: World War I, the recovery from the Great Depression, World War II, the Great Recession (2007-2009), and then the unprecedented fiscal response to the COVID-19 pandemic.

Historically, the U.S. reduced its debt-to-GDP through rapid economic growth, spending restraint, or higher inflation. After World War I, reduced spending and large tax collections (including high tariffs under Warren G. Harding and Calvin Coolidge) reduced this ratio. The rapid economic expansion following World War II, with a young workforce, a manufacturing boom, and limited entitlement spending, helped. In the 1990s, bipartisan budget agreements and a strong economy stabilized the debt.

Why did the steady 20+ year decline in debt after World War II end in the 1970s and turn upward?

First, the U.S. left the gold standard (Bretton Woods, 1971), causing economic instability and inflation—which contributed to a state of “stagflation” (low GDP growth, high inflation, and unemployment). When campaigning for president, Jimmy Carter dubbed this the “misery index,” then, as President went on to drive the index even higher.

Furthermore, because of American dependency on foreign oil, supply shocks drove a recession. Entitlement programs began to grow rapidly (Medicare and Medicaid were created in 1965), further adding to expenditures that grew thereafter. Then, in the 1980s, the Cold War military build-up and tax cuts without sufficient spending cuts created an ongoing situation of yearly deficits that have added to our debt nearly every year since.

If debt were alcohol, the United States is suffering from a massive hangover after a nice party. Entitlement programs consume a far larger share of the budget than ever, the workforce is aging, and political incentives reward short-term spending over long-term prudence and stability. Much of the burden to pay down this debt will lie with our children—the ones currently too young to vote.

While we hear a lot of talk from Washington about addressing deficits and debt, nothing substantial has changed.

What the Future Looks Like

The bipartisan Congressional Budget Office (CBO) projects that debt will continue rising. by 2036 interest payments alone will be $2 Trillion—about 5% of the U.S. GDP—while the 2036 deficit (added to debt) will be another 7% of GDP. Demographics, healthcare costs, and interest payments are the primary drivers. If interest rates remain above economic growth rates (and they normally do), debt will compound faster than the economy can keep up—think of a debt spiral scenario.

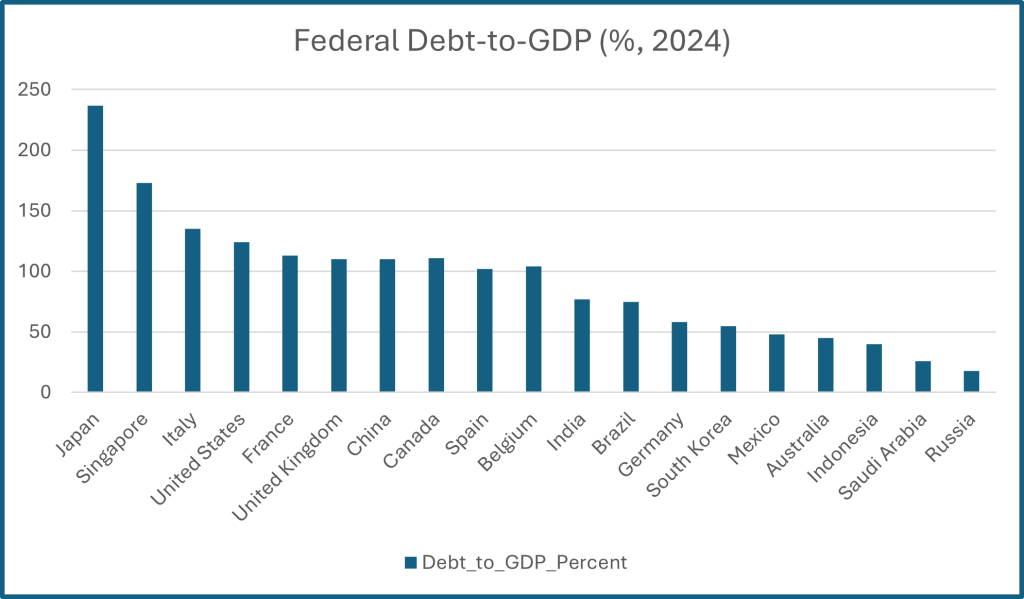

There is no precise tipping point at which debt becomes insurmountable, but most research suggests that once debt exceeds 100–120% of GDP, risks increase significantly. Sustainability depends on investor confidence, interest rates, economic growth, and the dollar’s reserve currency status. Japan has sustained higher ratios, but its domestic savings patterns and political economy differ dramatically from America’s.

The U.S. cannot assume unlimited borrowing capacity.

What Could Trigger a Fiscal Crisis

A fiscal crisis doesn’t require outright default on debt. It can emerge through rising interest rates, persistent inflation, a weakening dollar, or a sudden loss of confidence in Treasury markets. Other nations have experienced sudden fiscal crises even when their debt seemed manageable, especially if confidence evaporates. The United States is not immune.

Paths Toward Stability

Stabilizing the debt requires a combination of spending restraint, entitlement reform, and pro-growth policies. Revenue options exist. We can broaden the tax base, simplify the code, close loopholes, etc., but the issue is more likely Washington’s spending problem.

Reforming Social Security and Medicare, reducing wasteful discretionary spending, reevaluating defense commitments, and introducing market competition into healthcare are essential steps.

Growth-oriented strategies like deregulation, high-skilled immigration reform, productivity-enhancing infrastructure projects, and workforce modernization can help expand the economic base that supports the debt.

Most importantly, incentives matter. If politicians were to get zero salary unless there is a balanced (or surplus) budget, things would be remedied quickly.

What This Means for South Carolina

For residents of South Carolina, the implications of rising federal debt are concrete and personal.

Higher taxes are a real possibility as future Congresses search for revenue. Working families and small businesses would feel the impact. Federal spending cuts could affect South Carolina military installations, infrastructure projects, and disaster relief/resilience. Inflation is eroding purchasing power, and South Carolinians already face rising costs for housing, insurance, and energy. Military communities are particularly vulnerable. Budget stress could influence base operations, military pay, local contracting, and long-term defense investment. These local economies would be deeply affected by federal spending decisions.

Individuals can take steps to prepare: reduce personal debt, save, diversify savings, support local businesses, and engage in advocacy for fiscal responsibility.

A Call to Action for South Carolinians

The U.S. Debt-to-GDP ratio now exceeds 120% and continues upward. The current trajectory reflects structural imbalance, political avoidance, and a federal government that has grown far beyond its constitutional scope. Without reform, South Carolina residents will face higher taxes, inflation, and more economic uncertainty.

Most of us value the principles of small government, fiscal discipline, and personal responsibility. Our state government, the primary area of work for Palmetto Promise, must balance its budget annually.

Now is the time to demand that elected officials adhere to these principles and do what most states do every year.

Below are some messages you can send to South Carolina’s congressional delegation. Feel free to adapt them to your own voice.

Message 1: Demand Fiscal Responsibility. “Please reduce federal spending, reform entitlements, and impose budget discipline. The current debt trajectory threatens economic stability and burdens future generations.”

Message 2: Oppose Unfunded Spending. “I urge you to oppose any new spending that is not fully offset. Congress must stop adding to the national debt without accountability. If a project does not have a positive social or economic return on its investment, do not fund it.”

Message 3: Support Pro-Growth Policies.Please advance policies that encourage economic growth, like deregulation, tax simplification, and market-driven healthcare reforms. Economic growth is essential to our ability to reduce the debt.”

Message 4: Protect South Carolina’s Economic Interests. “As a resident of South Carolina, I am concerned about how rising federal debt will affect military communities, small businesses, and working families in the Palmetto State. Please prioritize long-term fiscal sustainability.”

Message 5: Demand Transparency. “Support measures requiring clear reporting of unfunded liabilities, long-term fiscal projections, and our reliance on foreign lenders. Voters deserve honest accounting. We must stop denying the unsustainable debt situation and kicking the can forward to future generations.”

Perhaps they will see the light if they feel the heat.

For other scholarly articles on the principles of freedom and liberty from Palmetto Promise Fellow Dr. Kevin Boeh, please visit his author page here.