House Agrees to $309M Senate Income Tax Roll Back, Cuts Overtime & Bonus Taxes, Too

South Carolina taxpayers were the winners this week in a friendly game of chicken between the Senate and the House over how deeply to cut the state’s top marginal individual income tax rate.

But before we get to the details of a busy money week for the legislature, here is a short tax cut history.

Fiscal History

Palmetto Promise Institute has called for comprehensive tax reform since our founding. During those roughly ten years, PPI has released some of the most comprehensive analyses on the subject. For over a decade, we saw no movement in response to our research. But suddenly, the large “7” displayed on every tax rate map for South Carolina, indicating a whopping 7% top marginal income tax rate—among the highest in the country—began to be seen for the Scarlet “A” it was.

The reform started tentatively. The 7% top rate became 6.5%. Then it trickled down incrementally to 6.0%. But in 2025, the dam finally broke. Legislative leaders and the Governor called for a transformational cut that would, with revenue growth, eventually lead to a 0% rate. Earlier this year, Governor McMaster, who had called for “speeding up” rate cuts, asked for aggressive income tax reduction in his final State of the State Address, promising to sign a bill eliminating it “…the second it arrives on [his] desk.”

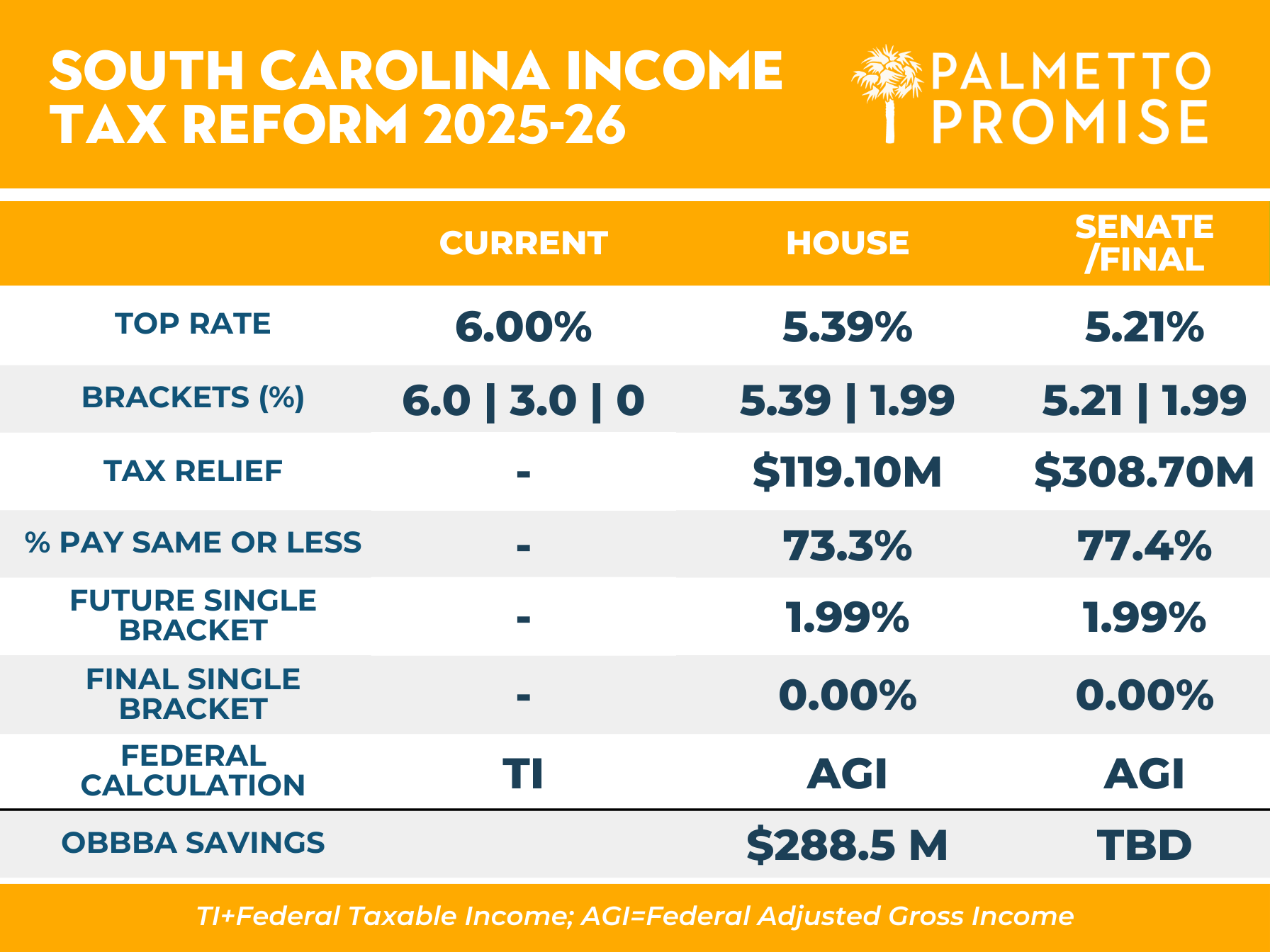

The legislation, H. 4216, which passed the SC House last May, shifted South Carolina from a 0%/3%/6.0% 3-bracket structure to a 1.99%/5.39% 2-bracket mechanism. (That’s down from five brackets and indexed to inflation, reforms that were completed in 2022.)

Senate and House

But, out-cutting the Senate was never likely, and the Senate had more fiscal projections to draw on. The Senate’s proposed changes, passed by that body on February 25, lowered the top tax rate further to 5.21%.

On Tuesday, the House accepted the Senate’s deeper cut and sent the bill to the Governor.

As the above graphic shows, tax relief went from about $119 million to about $309 million, which also increased the percentage of citizens paying the same or less from 73% to 77%. (Those paying more are mostly among the 44% of residents who were paying no taxes at all previously. Under the new rates, most everyone will have some skin in the game.)

An Adjacent Fix

As we have written, South Carolina’s current income tax system is not only complex, and uncompetitive, it has also been tethered to an ill-representative federal tax policy. By moving from federal taxable income (TI) to federal Adjusted Gross Income (AGI) as the starting point for state taxation, H.4216 brings sovereignty and predictability to South Carolina’s tax system.

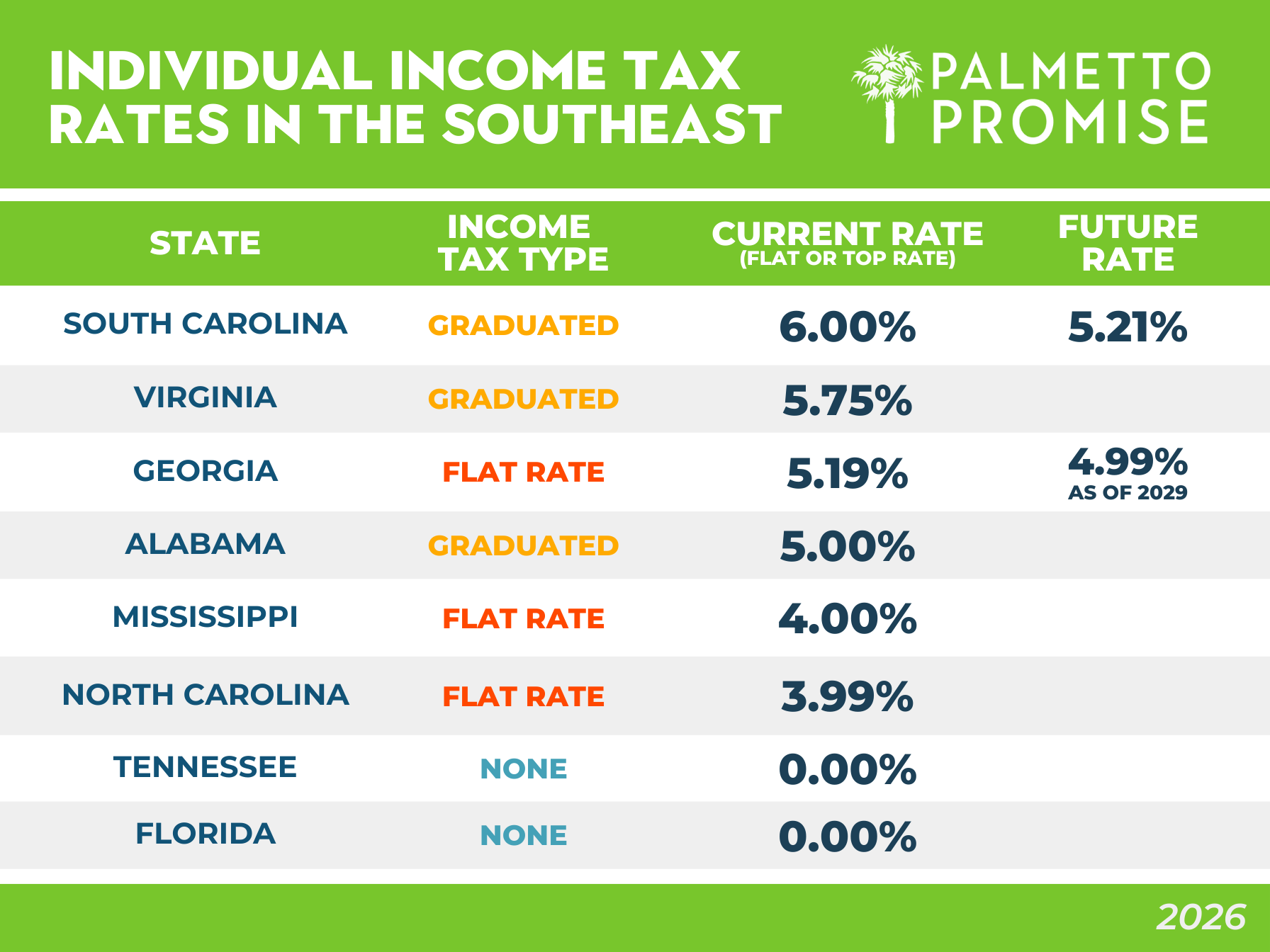

Historically, our reliance on federal tax standards has burdened our state with higher rates than our neighbors because these external standards are ill-suited to South Carolina. Our effective rate (what average citizens actually pay in income taxes) has been competitive for years, but there was that Scarlet A. In neighboring states, income tax rates are lower or scheduled to be dropped further or both. For instance, North Carolina has a flat income tax of 3.99% (2026), and Georgia is at 5.19% (2026). Georgia is expected to drop to 4.99%. Tennessee and Florida have no income tax at all.

Lower Rates Encourage Growth

Replacing the current multi-bracket structure with a streamlined two-rate system—and eventually a flat one-rate system (1.99%, then 0%) moves South Carolina closer to a tax code that families can understand and businesses can plan around—reducing compliance costs, incentivizing planning, and diminishing uncertainty.

South Carolina’s top marginal rate for income tax has historically placed us at a competitive disadvantage relative to many neighboring states, disincentivizing external investors and prospective businesses. Lowering rates sends a signal that South Carolina is welcoming to workers of all collars. Research shows that lower marginal income tax rates can enhance economic growth, increase labor force participation, and attract new investment. Palmetto Promise analysis, crafted with assistance from the Buckeye Institute, projected that the original House bill would create 1,000 jobs per year.

Revenue Based Structure & Fiscal Responsibility

Utilizing a revenue-based approach to income tax better enables legislators to lower rates more easily in the future. Lasting tax reform such as this must be anchored in responsible budgeting and prudent spending if we want to fully realize its long-term effects. Our state lawmakers should prioritize spending restraint and the protection of reserve funds to ensure that rate reductions are durable. If paired with fiscal discipline, H.4216 can help position South Carolina as the most economically competitive state in the Southeast.

Other Tax Cut Opportunities

The General Assembly is not finished with cutting taxes. In fact, immediately after passage of the annual state appropriations bill and capital projects bill, the House passed legislation conforming South Carolina to the portions of the federal One Big Beautiful Bill (OBBBA), most notably excluding Overtime Pay and Bonuses from Taxation (H.3368). Fiscal analysts project Individuals and Corporations to save $288.5 million in state taxes (2026-27) due to this conformity.

The Senate and House have other tax cut plans as well. The House has already passed H.5006, State of South Carolina Small Business [Property] Tax Cut of 2026,” which removes business personal property taxes for the first $10,000 “of net depreciated value of business personal property.”

The Senate, in turn, has passed S.768, which creates a new property tax exemption for citizens who have been residents of the state for five/ten years (two levels of tax relief) and have paid property and income taxes during those periods of time. This bill has not been taken up in the House (yet).

The Bottom Line

We have not arrived at comprehensive tax reform. But what could be designated “Tax Cut Session 2025-26” represents meaningful progress toward a tax system that is simpler, flatter, and more growth-oriented. With careful refinement and commitment to fiscal responsibility, these reforms could help businesses flourish and families thrive in South Carolina.

As for us, we are hoping for victory on all fronts.

Finally, let’s remember that we should not take these cuts for granted. It has been a long road to this point, and as South Carolina is cutting, other states are raising taxes.

On to comprehensive reform.

________________________

Note: This was finance week in the South Carolina House. In addition to the individual income tax cut, the state appropriations bill, and the removal of overtime and bonuses from taxation, Capital Reserve Fund appropriations [H.5127] passed.

This bill featured the shortest list of capital projects in memory with virtually all funds available in that account appropriated to a new Comprehensive Cancer Hospital at the Medical University of South Carolina in Charleston ($175 million), the DOT for bridge repair and upgrades (about $140 million), and the Adjutant General for state matching funds to receive federal disaster assistance ($72.80 million). We will have more to say about the state appropriations bill in a future post.