Santee Cooper’s Debt is Still Shaping South Carolina’s Power Bills

On July 31, 2017, construction was halted on the V.C. Summer Units II and III nuclear expansion project in Fairfield County. One of the entities responsible for the project’s failure was South Carolina’s state-owned utility, Santee Cooper. After the debacle, Santee Cooper and its V.C. Summer co-owner, SCE&G (now subsumed by Dominion Energy) assumed billions in debt from the failure of the project. SCE&G turned to ratepayers and to Investor-Owned Utility (IOU) Dominion to cover the losses. Santee Cooper, as an arm of the state, had no investors, so ratepayers are taking the hit. The utility was sued for mismanagement, leading to the Cook settlement that included a 5-year rate freeze that began in 2020. But much of the debt remains. This, while Santee Cooper is at risk of falling behind on capital infrastructure projects to meet growing demand from data centers and population growth, both in its direct-serve territory and that of the rural electric co-ops that depend partially on Santee Cooper for electricity.

This raises one basic question: how much debt is Santee Cooper carrying, and is it too much?

In 2017, Santee Cooper and its partner SCE&G abandoned the two nuclear reactors after spending $9 billion on the project, which was never completed. As of late last year, Santee Cooper still had $3.6 billion in V.C. Summer debt, an amount that ratepayers have continued to pay each month. CEO Jimmy Staton has acknowledged this burden, stating it is time customers saw some value through efforts to salvage the V.C Summer project through a proposed sale to Brookfield Asset Management.

How much debt does Santee Cooper really have?

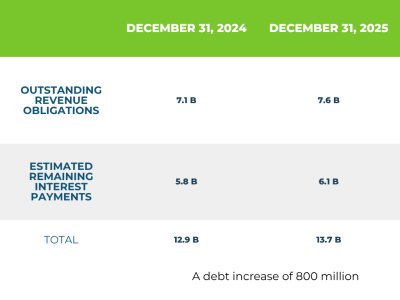

According to Santee Cooper’s most recent Annual Report to Fitch and Moody’s early-2026 reports, Santee Cooper has $7.5-$7.6 billion in revenue bond debt, scheduled to be repaid through 2056. When interest is included, the total repayment could reach $12-15 billion by maturity. It also has $400 million in short-term borrowing from bank credit.

Santee Cooper’s debt is not expected to decrease anytime soon. Santee Cooper’s plan to spend $5.9 billion on capital investments to support transmission and resource spending is more than double the $2.2 billion spent in the previous five-year period.

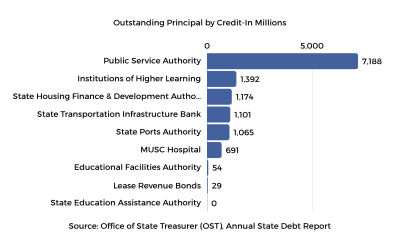

For comparison purposes, the Office of State Treasurer (OST) Annual Debt Report shows

The average level of revenue bond debt is not in the same ballpark with Santee Cooper debt (listed by its formal name here, “the South Carolina Public Service Authority”), and the next highest debtors—enormous state agencies—are at around $1 billion in debt, just a bit more than the 2024-25 debt increase at Santee Cooper.

Customers feel this debt directly through monthly bills. In spring 2026, Santee Cooper’s board approved rates to increase by 4.6% starting in February 2027, followed by 4.8% in 2028. Industrial and commercial customers would see increases of between 2.1% and 2.9%.

One deal could reduce the utility’s debt load. Brookfield Asset Management, an investment firm, is looking to restart construction of the partially built reactors. The $2.7 billion exchange is an arrangement intended to pay down the utility’s debt. Santee Cooper would retain ownership of up to 25% of the two reactors, giving customers future access. However, the deal is far from done. It is dependent on due diligence studies and licensing approvals, with no set timeline and no payment expected for at least two years. Until then, the debt remains on ratepayers’ bills.

Lessons from Georgia

South Carolina’s neighbor has a similar story, but a different outcome. Plant Vogtle is owned by Georgia’s Municipal Electric Authority (22.7%), electric co-ops (30%), and the IOU Georgia Power (45.7%). Each contributed to the expansion of the Plant Vogtle nuclear plant and took on billions of dollars of debt to pay for the nuclear reactors. There was no Santee Cooper-like entity involved, owning 45% of the project, like with V.C. Summer II and III. (Santee Cooper currently owns 100% of the unfinished reactors. V.C. Summer I has an ownership split of 2/3 Dominion and 1/3 Santee Cooper.)

Georgia finished its project, with both reactors producing electricity and generating revenue now. Both South Carolina’s and Georgia’s AP1000 projects experienced significant cost overruns. But Georgia has working, revenue-generating nuclear reactors, while Santee Cooper’s customers are still paying debt on a project that never produced a kilowatt of electricity.

The Bottom Line

Santee Cooper has about $7.5 billion in outstanding bonds today, with interest continuing to accumulate, while the utility’s customers are paying for it. With at least $4.3 billion in additional borrowing planned, and a $2.7 billion debt V.C. Summer payoff is still uncertain because the Brookfield deal remains unfinished, Santee Cooper’s debt load is set to grow before there is any prospect of it shrinking significantly.

With Dominion merging with NextEra Energy, it could be time for another round of discussions on the sale of the tiny utility to an Investor-Owned Utility that would be in a position to take advantage of economies of scale and get co-op and direct serve customer bills down.