South Carolina’s Hidden Tax: How Manufacturing Property Taxes Could Threaten Our State’s Growth

When citizens debate the dreaded subject of taxes, the conversation nearly always revolves around individual income taxes. This was a hot topic in the 2025 South Carolina General Assembly. Yet, behind the scenes, another stealthier tax is quietly shaping the state’s economy just as powerfully: the manufacturing property tax. South Carolina has historically lived on the edge in terms of economic development by having some of the highest manufacturing property taxes among the 50 states. Currently, South Carolina has the 6th highest manufacturing property tax rate in the country.

It is no surprise that high manufacturing property taxes deter major employers from establishing operations in our state. However, South Carolina is finally making strides toward mitigating this tax. In May 2025, the South Carolina Senate quietly passed S.439 (sponsored by Senate Finance Committee Chairman Harvey Peeler, R-Cherokee), a property tax reduction bill that expanded the previously passed Act 288 (2022). The idea behind Act 288 and S.439 is the concept of a “PVE” or “partial value exemption.” More about that shortly.

S.439 now rests in the House Ways and Means Committee, and in a 2026 session that is expected to yield conversations about comprehensive tax reform, the manufacturing tax fix that S.439 represents could be in play.

What are Manufacturing Property Taxes and Who Pays Them?

The Tax Foundation defines a property tax as a tax “on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services.”

But how is a “manufacturer” defined? Put another way, what businesses are subject to the manufacturing property tax? The South Carolina Department of Revenue explains that the manufacturing property tax “applies to owners of all real and/or personal property owned, used or leased by Manufacturers, Mining Companies or Industrial Development Projects.” The definition of manufacturing, particularly in Act 228 and S.439, does not include utilities.

To calculate the specific property tax for each manufacturing facility, South Carolina has a complicated and costly method of crunching those numbers. The SC Chamber’s South Carolina Property Tax Study reveals this process:

- An assessment is conducted of the property to determine its appraised value.

- The value is then multiplied by the assessment ratio of 10.5% stated in the South Carolina Constitution to determine the assessed value.

- Lastly, the manufacturing property tax bill is calculated by multiplying the property’s assessed value by the total millage rate, which combines the tax rates from the county, city, school district, and other local taxing authorities.

Historically High Manufacturing Taxes

Not only is this system convoluted for manufacturers, but the resulting tax burden is high. The assessment ratio for manufacturing is one of the highest ratios for property in South Carolina. The following table shows the assessment ratios for the various types of property in our state.

Manufacturing, utility, and personal business properties have the highest assessment ratios, meaning that these property owners must pay the largest tax rate on their property. One may think that the easiest solution would be to change the assessment ratio. However, because these percentages are written in the state constitution, South Carolina cannot change the ratio without altering the constitution. To amend the constitution, two-thirds of representatives must approve it in the House, and two-thirds of senators must approve it in the Senate. Once the proposed amendment passes both chambers, the amendment goes to the people in the next General Election. Then the same legislative process must occur for ratification of the new amendment. To circumvent that arduous process, over time, the General Assembly has developed workarounds to lower the property taxes on manufacturers. S.439 takes this route.

What is Act 228?

To decrease the burden of property taxes for manufacturers, the South Carolina General Assembly amended Section 12-37-220 of the SC Code of Laws in 2022 to create a “partial value exemption” or PVE. This move, codified in Act 228, means the state in essence pays the jurisdictions assessing the tax a rebate. This buy-down is intended to attract businesses and manufacturers to our state, as manufacturers will not be on the hook for the entire assessed property tax. Instead, they pay only 42.8571% of their property tax calculated with the steps explained above.

Because after 2022 manufacturers do not pay the full amount of property taxes, there is a loss of local revenue that would have been put towards schools and other needs funded by the property tax. Consequently, Act 288 offsets this loss by providing the local governments with up to $170 million per year statewide. That $170 million is sourced from state funds received from other taxes. If the revenue loss is ever projected to be larger than $170 million, then the property tax that manufacturers pay will increase proportionally.

What does S.439 do?

At first blush, it might be assumed that the purpose of S.439 would be to increase the manufacturing property tax buydown (“PVE”) even further, but this is not the case. S.439 does not decrease the percentage of taxes that manufacturers pay on their property; that 42.857% will stay the same. Instead, this bill seeks to amend Section 12-37-220 of the South Carolina Code of Laws to increase the reimbursement “fund” from $170 million to $370 million per year. All of the provisions of Act 228 otherwise remain.

Importance of Amending Section 12-37-220

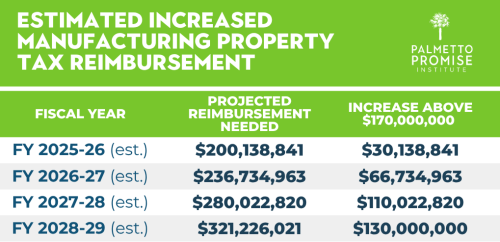

According to S.439’s fiscal impact statement, the South Carolina Revenue and Fiscal Affairs Office (RFA) projects that the reimbursement will pass $170 million by FY 2025-26, meaning that more South Carolina manufacturers will be taking advantage of all of the tax exemption fund, and that 42.837% will start to increase proportionally after the $170 million reimbursement cap is exhausted. While legislators did attempt to circumvent this with a proviso (temporary one year provision) in the 2025 budget, a permanent fix with S.439 is crucial to avoid an increase in the percentage paid for manufacturing property taxes and driving away business from our state. See the RFA table below to determine the projected reimbursement each year after FY 2024-2025.

In the Fiscal Impact Statement, RFA also released estimates of how the reimbursement will increase each year starting in FY 2025-26 in the event that S.439 passes. The cap of $370 million will not be automatically met for FY 2025-26 but will get there gradually. See the table above (third column) to also see the predicted yearly reimbursement increase in the event that S.349 becomes law.

Conclusion

When the General Assembly reconvenes in 2026, tax reform will be a major topic of conversation, and with some of the highest manufacturing property taxes in the United States on the books, the provisions of S.439 must be part of the discussion if we want to ensure South Carolina maintains economic competitiveness. S.439 means tax relief for job creators while keeping local governments financially stable through reimbursement funds that offset lost local revenue. Since legislators cannot change the assessment ratio without altering the state constitution, creating a tax cut by increasing the reimbursement fund is the best way for South Carolina to lower manufacturing taxes now before that $170 million cap is hit and manufacturers see a tax increase.

Close observers of the South Carolina industrial property tax framework will raise the question of FILOTs—Fees in Lieu of Taxes. Yes, FILOTs are available to a few firms who are lucky to be among the chosen to enjoy that property tax break, but all job-creators don’t make the popularity contest for the lucrative FILOT property tax reduction. That’s another reason why this permanent PVE fix is needed. Ultimately, bills like S.439 sustain the balance between tax relief and fiscal responsibility, ensure that South Carolina remains competitive for manufacturers, and put South Carolina in the frame for robust economic growth for years to come.

For more on the PVE and how South Carolina can achieve comprehensive tax reform in 2026, refer to Dr. Oran Smith’s January 2025 report Achieving Prosperity, Stability, and Fairness.